How To Automate Your Finances With The 3 Bank System

Imagine waking up, checking your bank account, and knowing exactly where every single penny is supposed to go without having to lift a finger. No more scrambling to pay bills on time. No more wondering where your hard earned paycheck disappeared to by the end of the month. If managing your money feels like a constant uphill battle, it is time to change your strategy. The secret to financial peace of mind is not necessarily making more money. Instead, the secret is setting up a foolproof system that manages your money for you. Welcome to the world of financial automation.

Automating your finances takes the emotion, the stress, and the manual labor out of building wealth. By creating a structure where your money flows logically from your employer to your bills, your savings, and your daily spending pocket, you can finally take control of your financial future. Today, we are going to dive deep into a proven, straightforward method that will revolutionize how you handle your income. We call it the Three Bank System.

The Golden Rule: Pay Yourself First

Before we get into the mechanics of multiple bank accounts, we have to talk about a fundamental shift in your money mindset. Most people follow a very dangerous financial formula. They get paid, they pay their bills, they buy things they want, and then they try to save whatever happens to be left over. The problem with this approach is that there is rarely anything left over.

To truly build financial stability, you must flip that equation on its head. You need to pay yourself first. This means treating your savings and your future investments like they are your most important monthly bills. When your salary hits your account, a predetermined portion should immediately detour into your savings before you even have a chance to look at it. This simple psychological trick guarantees that you are consistently building a safety net, regardless of what other temptations pop up during the month.

The Core Philosophy: Give Every Pound a Job

Another crucial element of automating your finances is the concept of giving every single unit of currency a specific job to do. When money sits in a massive, undivided pile in one checking account, it is incredibly easy to accidentally spend your rent money on a weekend getaway. Your brain sees a large balance and assumes you are rich.

By giving every pound, dollar, or euro a designated purpose, you remove the guesswork. Some money has the job of keeping the lights on. Some money has the job of protecting you in an emergency. And some money has the highly enjoyable job of paying for your daily coffees, dinners out, and entertainment. When every coin has a mission, your financial life becomes a well oiled machine.

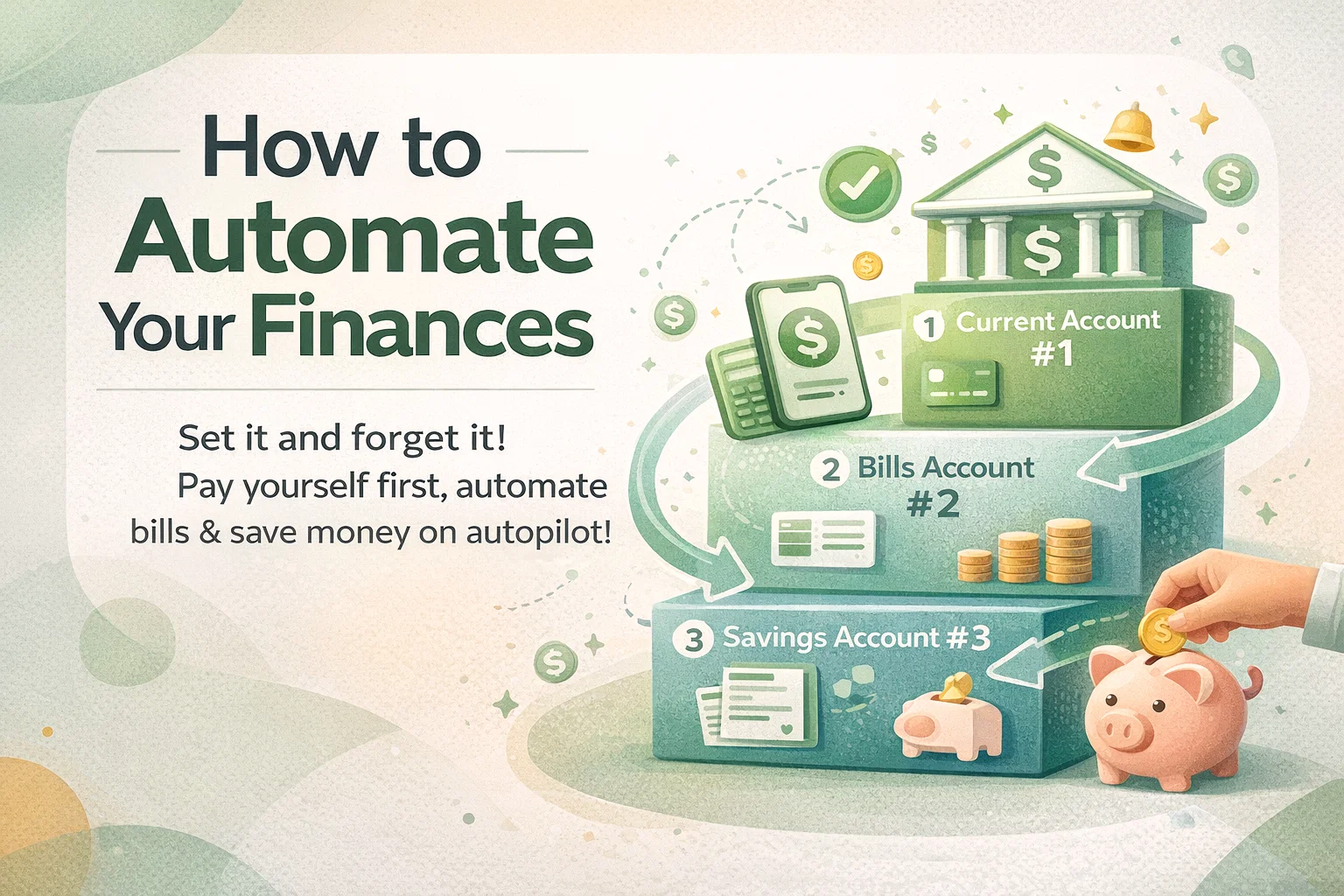

Introducing The Three Bank System

To put these philosophies into practice, you need the right infrastructure. Relying on sheer willpower and a single checking account is a recipe for disaster. This is where the Three Bank System comes in. By utilizing three distinct accounts, you create physical boundaries for your money. Let us break down exactly how this setup works and why it is so wildly effective.

Account Number 1: The Daily Spender

This is your primary current account. It acts as the grand central station for your finances. This is the account where your hard earned salary lands on payday. However, it is vital to understand that the money does not stay here for long.

Once your salary lands in Account Number 1, the automation magic begins. Money is immediately sent out to your other designated accounts. We will cover those in a moment. What remains in Account Number 1 is your safe to spend money. This is your allowance for the month. It covers your groceries, your fuel, your shopping trips, and your social life.

Crucially, this is the only account that you carry a physical debit card for. You should also connect this account to your mobile wallet apps like Apple Pay or Google Pay. Because all of your serious responsibilities are being handled elsewhere, you can spend the money in this account completely guilt free. When the balance hits zero, you stop spending until the next payday. No dipping into savings allowed.

Account Number 2: The Bill Payer

Your second account is another standard current account, but its purpose is strictly utilitarian. This is your dedicated bill paying hub. All of your fixed, predictable expenses live here. We are talking about your rent or mortgage, your utilities, your council tax, your gym membership, your car insurance, and your streaming subscriptions like Netflix or Spotify.

Here is the most important rule for Account Number 2. You must never, ever carry the debit card for this account in your wallet. In fact, if you can avoid having a card for it altogether, that is even better. You can download the banking app to monitor the balance, but this money is untouchable for daily spending.

By isolating your bill money from your spending money, you eliminate the risk of accidentally spending your rent. You will sleep soundly knowing that no matter how many coffees you buy from Account Number 1, the money required to keep a roof over your head is sitting safely in Account Number 2, waiting for the direct debits to pull it out.

Account Number 3: The Wealth Builder

The third pillar of this strategy is your High Interest Savings Account. This is where your financial security grows. This account houses your emergency fund and your savings for specific short term goals, like a vacation or a new car deposit.

To maximize the effectiveness of this account, you need to create what financial experts call a spending speed bump. This means the money should not be instantly accessible. Do not keep this savings account with the same bank as your daily spender account. If you can transfer money from savings to checking with a simple swipe on your phone while standing in line at a clothing store, it is too easy to sabotage your goals.

Instead, choose a different institution for Account Number 3. Make it so that accessing these funds requires logging into a different website, waiting two business days for a transfer to clear, or even having to make a phone call. This deliberate friction gives your logical brain time to catch up with your impulse buying brain, saving you from regretful purchases.

Leveling Up: The Bonus Investment Account

Once you have mastered the Three Bank System and you have successfully built up a fully funded emergency reserve, usually three to six months of basic living expenses, you are ready for the bonus round. It is time to open an investment account.

Leaving large sums of cash in a traditional savings account for the long term is actually a surefire way to lose purchasing power due to inflation. To truly grow your wealth, you need to invest. Setting up a dedicated investment account, such as a brokerage account or a retirement wrapper, allows your money to work for you.

Keep it simple. You do not need to become a Wall Street day trader to be successful. Look into low cost, broadly diversified index funds. These funds track the overall market, providing steady, reliable growth over the decades. Just like your savings, you should automate your contributions to this account every single month.

Your Step by Step Guide to Automating Your Money

Understanding the theory is great, but taking action is what actually changes your life. Here is exactly how to implement this system today.

- Step One: Calculate your fixed costs. Sit down with your last three months of bank statements. Add up every single recurring bill. Rent, insurance, phone bills, internet, debt minimum payments. Calculate the exact total you need to survive each month.

- Step Two: Open your accounts. If you do not already have them, open your second current account for bills and your high yield savings account at a separate bank.

- Step Three: Route your income. Ensure your employer is depositing your full paycheck into Account Number 1.

- Step Four: Schedule the transfers. This is the most critical step. Log into Account Number 1 and set up two recurring, automatic transfers to trigger the day after you get paid. The first transfer sends your total fixed costs amount to Account Number 2. The second transfer sends your savings goal amount to Account Number 3.

- Step Five: Automate the bills. Log into all of your service providers, your utility company, your landlord portal, your credit card companies. Set them all up to automatically pull their payments via direct debit exclusively from Account Number 2.

- Step Six: Set up alerts. To keep things running smoothly, set up balance alerts on your accounts. Get a text message if Account Number 2 drops below a certain threshold to avoid any surprise overdraft fees.

Budgeting Like a Boss

Automation handles the heavy lifting, but you still need to be the visionary director of your financial life. This requires regular check ins and a solid budgeting framework. You do not need to track every single penny obsessively, but you do need a big picture overview.

Find a tool that works for your personality. This could be a customized spreadsheet that you update weekly, or a dedicated budgeting app that syncs with your accounts. The tool itself matters less than the habit of using it.

Make a date with your money once a month. Pour a cup of coffee, sit down, and review your spending. Did you blow past your dining out budget in Account Number 1? Do you need to adjust the amount you send to Account Number 2 because your internet bill went up? Tracking your spending allows you to adjust your automated transfers so they perfectly reflect your current reality and your future goals.

Conclusion: Your Roadmap to Financial Freedom

Taking the time to set up an automated financial system is one of the highest return investments you will ever make in your own wellbeing. By utilizing the Three Bank System, you are effectively protecting yourself from your own worst spending habits. You are ensuring your bills are never late. You are guaranteeing that your savings grow month after month.

It might take a few hours this weekend to calculate your numbers, open the necessary accounts, and schedule your automated transfers. But once that initial work is done, the system runs itself. You get to step back and enjoy the peace of mind that comes from knowing your money is finally working for you, rather than the other way around. Stop relying on willpower. Start building your automated wealth machine today, and watch as your financial stress simply melts away.